Activity is slowing, more volatile and with starkly different characteristics across regions. Growth has surprised on the upside this year, but signs of slowing are becoming more evident. Conditions should be far weaker next year as delayed constraints from higher interest rates and less generous fiscal spending weigh in consumption. Manufacturing has been weak for a year and the post-pandemic surge in pent-up services activity like travel and entertainment is beginning to subside.

Bank lending volumes are turning lower in various regions thus curtailing growth projects. Sensitivity to higher interest rates is different across countries depending on the structure of housing and lending markets. A reasonable proportion of tighter monetary policy is still to be felt. Lower income households are most vulnerable to the tougher conditions given less stable work engagements, particularly as the substantial savings built during the pandemic are being run down.

The US economy, which has grown amongst the sharpest, perhaps has the furthest to fall. Its central bank has been the most dynamic inflation fighter and has lifted rates more clearly into restrictive territory than others. A recession may be necessary to force wages and broader inflation down to target levels through higher unemployment. The US then may be among the first to have pressure released through lower rates, probably in the second half of next year.

Europe may already be in recession, beset by the aftermath of the energy crisis, export weakness and low consumer confidence. In contrast, China’s economy may be starting to improve as post-lockdown travel and consumer spending cautiously lift while selective government stimulus helps contain troubles in the property sector.

Slowly receding inflation complicated by higher energy costs

Core inflation has declined from peak levels but remains well above central bank targets. Cost pressures have declined in goods markets but remain elevated for services due to strong wages gains and built-up post-pandemic demand for personal interactions. It may take more than a year yet for price increases to recede to central bank target levels. Softening labour markets are key but higher energy costs add complications.

US inflation may not fall to target levels until at least the end of 2024, but softening consumer and fiscal spending will assist this process. European inflation is also unlikely to recede quickly despite far softer economic conditions, particularly if heightened inflation expectations are built into wage agreements.

In contrast with many other countries, higher inflation in Japan can be seen as constructive for the economy following the many years of deflationary patterns since the 1990s. however, general price rises should fall back below 2% once more by mid next year particularly if wages growth remains subdued. In Australia, inflation may remain above the target band until 2025 due to relatively strong wages and rent growth and a central bank that has been less assertive on rates than others.

While declining in time, inflation can be expected to be volatile in the next several years as companies continue to rationalise and diversify supply chains to preference certainty of supply over low cost. Geopolitical tensions and climate change challenges add to complexity. The globalisation goal is diminishing while various governments are showing a willingness to run large budget deficits and intervene in several industries in order to offset cost-of-living challenges. Meanwhile, the events in the Middle East have prompted further volatility in energy markets and increase risks of supply shocks for the global economy.

Central banks to shift to easing cycle next year

Major central banks have lifted rates substantially in the last year or so and are likely to at least hold these levels while inflation declines sustainably to around target levels. A further shift into restrictive territory is possible in the US to ensure that underlying activity softens enough. There are few signs of slowing in the US jobs market yet. Initial claims for unemployment benefits have not budged. The pace of job creation has moderated, but the 150,000 created in October 2023 was still more than usual.

While policy in the US is more clearly restrictive with cash rates at 5.25-5.5%, this is not the case in other countries. The cash rate adjusted for inflation (or, real cash rate) is around +1.5% in the US while it is around zero in Europe, -1% in Australia and -3.5% in Japan.

The European Central Bank is likely to face calls to cut rates from 4% in the face of weak activity across the region, but it will likely wait until the middle of next year when inflation should be significantly lower. By maintaining extraordinary monetary stimulus, Japan’s approach has been distinct from others. The Bank of Japan has feared dampening activity too quickly. It is likely to progressively allow more flexibility in longer term government bond yields over the next year following a first step in this direction a few months ago. Recent elevated inflation readings in Australia should encourage at least one more rise in rates in the next several months to where they may be held for an extended period.

Investment Strategy

High market volatility can be expected for some time yet. It is therefore wise to carry in portfolios a larger than usual weighting to cash which offers a reasonable return on its own due to the recent lift in interest rates. Tighter financial conditions such as through higher long term bond yields, oil prices and the US dollar can increase stresses within markets. There are vulnerabilities within private credit and commercial real estate internationally.

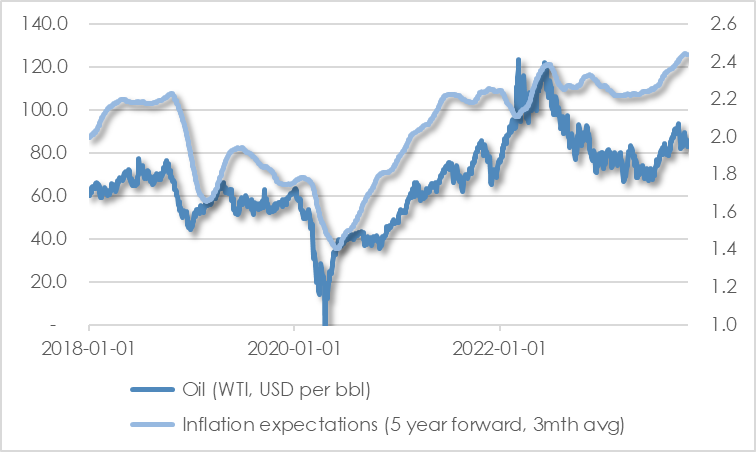

Oil prices are more than 20% above levels in the middle of the year as supply concerns offset the likelihood of weaker demand in the next year. Inflation expectations have lifted noticeably in that time, prompting a further rise in longer term bond yields.

New borrowers and those with debt maturing will now pay more. Higher US yields encourage a stronger US dollar which weighs on commodity prices and increase challenges for emerging market economies. All this while labour markets are softening. Unsurprisingly, consensus earnings forecasts are being revised lower.

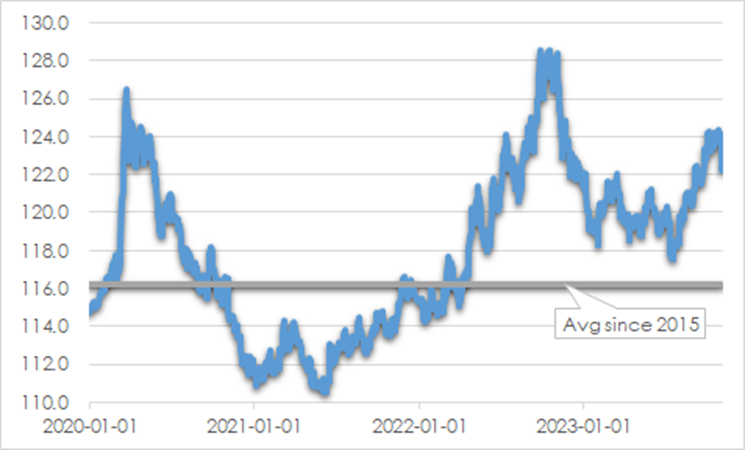

CHART 1: US TRADE-WEIGHTED INDEX

Source: Board of Governors of the Federal Reserve System

CHART 2: OIL VS INFLATION EXPECTATIONS

Source: St Louis Fed, AssureInvest

Fixed interest assets still offer little outright value despite the recent rise in yields. The Reserve Bank of Australia’s slowness in clamping down on inflation means yields may be higher for longer. We remain underweight the fixed interest asset class and with shorter duration than benchmark along with only modest weighting to mainly higher-quality credit securities.

Recent market drawdowns mean there are increased opportunities for careful investment in growth assets. However, no more than a neutral allocation relative to strategic asset allocations can be justified to the overall equities asset class. Valuations remain reasonably full, and markets are likely to be surprised by the duration of tighter monetary policy and the weight on corporate earnings from softer discretionary demand and improving yet still problematic cost escalation.

In regional equity allocations, we see more value in Europe, Japan and Australia where valuations are more favourable and monetary policy is likely to be less punitive. Europe should benefit sooner than most from a shift to more supportive measures. Despite the high presence of some of the world’s most wonderful businesses, US equities have far less favourable valuations and have more exposure to a domestic economy likely to soften more dramatically than many given the need for restrictive policies to eventually cool hot jobs markets and wages growth.

In direct equities portfolios, the focus remains on internally funded, strongly cash generative businesses with enduring competitive advantages and long growth runways that will fare better than others while economies soften. Purchasing entities like these at attractive valuations should support wealth generation in time. Higher dividend yields are also an attractive component of total investor return given the challenges associated with capital growth in the forecast horizon.

We see particular value in several healthcare companies overly beaten down on company-specific issues and some uniquely-positioned consumer discretionary firms where the market has overreacted to near term demand weakness.

Andrew Doherty. AssureInvest

The Information constitutes only general advice to wholesale investors. In preparing this document, AssureInvest did not take into account your particular goals and objectives, anticipated resources, current situation or attitudes. Before making any investment decisions you should review the product disclosure statement of the relevant product and consult a securities adviser. Past performance is no guarantee of future performance. This document is not intended for publication outside of Australia.

FREE Special Report: How to Jump ahead of competitors and add more value for clients

Learn how you can boost profits while enhancing customer outcomes.