When it comes to designing the ideal portfolio for any investor, one size does not fit all. An ad-hoc approach to allocating across different asset classes risks reducing the ability of the investor to fund their retirement and lifestyle needs.

A well-managed multi-asset portfolio brings the advantages of measured risk-taking within the individual investor’s risk tolerance, and enhanced returns through tactical asset allocation and instrument selection.

Strategic asset allocation is the process of designing the ultimate long-term asset allocation plan based on a range of personal factors including return goals and risk tolerance. These factors may change over time as the investor’s circumstances change.

Here we examine the key elements that are critical in determining the appropriate strategic asset allocation. We discuss how individuals define “risk” differently and how this impacts portfolio design, and we debunk an old rule of thumb that asset allocation should mirror the investor’s age.

“I will tell you how to become rich. Close the doors. Be fearful when others are greedy. Be greedy when others are fearful.” Warren Buffett

INVESTOR RISK PROFILE

In order to provide investment recommendations suited to an investor’s individual needs, advisors collect information on their financial situation, needs, goals and concerns. The investor profile questionnaire, completed in initial client meetings, facilitates this information exchange.

Establishing the client’s investment risk profile will determine the appropriate investment policy, or strategic asset allocation, through a series of questions aimed at discovering their investment time-frame, knowledge and experience, acceptance of asset price volatility, need for regular cash payments, their specific tax situation and preference for income or capital growth-style returns.

Growth-style assets like equities and property tend to rise in value faster over time than income-style assets like cash and bonds, but their asset prices also tend to swing around more vigorously. Other things being equal, the longer the investment horizon, the greater the justification for tilting toward growth assets as there is sufficient time for future gains to compensate for losses in any one year.

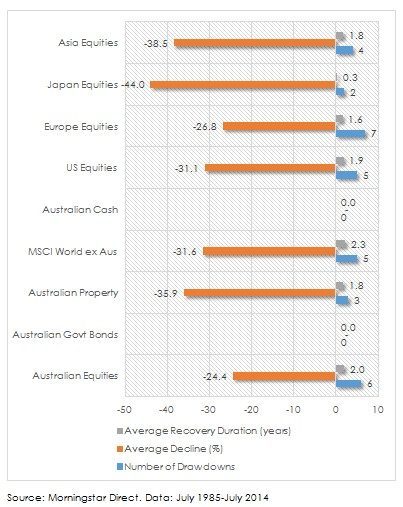

Australian equities, for instance have fallen 10% or more six times by an average of 24% in the past 20 years, and it has taken on average two years for the market to recover these drawdowns. Drawdowns of this magnitude have been experienced five times in the last 20 years for US equities and seven times for European equities and these have also taken around two years to recover.

Australian cash and Australian Government bonds have not experienced losses of this magnitude at any time in the last 20 years.

ASSET CLASS FALLS MORE THAN 10% AND RECOVERY PERIOD (1985-2014)

RISK DEFINITIONS

Each investor has a different definition of, and tolerance for, “risk” which will help inform the appropriate strategic asset allocation – the possibility of not meeting financial objectives, or preserving capital, or generating returns above inflation; the risk of undue volatility in asset prices, or the risk of outliving their retirement plan. Some investors are content to experience substantial short-term swings in the value of their assets, with the view that their value will rise over time. Others wish to reduce potential asset price swings.

Investors typically prioritise different types of risk. Naturally, most focus is on downside risk. Few investors agonise over their portfolio doubling! Instead they worry about making capital losses or experiencing below-average returns.

COMMON INVESTOR RISK HIERARCHY

Capital preservation is central to AssureInvest’s investment philosophy, as expressed in our long-term focus on attractively-valued, diversified high-quality assets. High-quality companies are less likely than others to face financial stress and they have greater capacity to generate superior and more reliable returns for shareholders over time. Nevertheless, while we take on less risk than the general market, the natural volatility possessed by growth assets like shares and property will not suit the most risk-averse investors.

Investors with greater knowledge and experience are more likely to suit portfolios with greater weightings to growth-style assets, given they are more likely to expect and accept the inherently greater volatility of these assets. Our enthusiasm for thorough explanation of our recommended investment positioning helps clients make informed investment choices suitable to their needs, including maintaining a weighting to growth assets that is appropriate considering their financial goals.

ASSET ALLOCATION SHOULD NOT MIRROR YOUR AGE

A popular asset allocation rule of thumb used by advisers has been to subtract the investor’s age from 100 to get their weighting to stocks, with the balance in bonds (and/or cash). According to this approach, the balance between stocks and bonds should be 60/40 at age 40, 40/60 at age 60, and so on. The concept here is that investors should take less risk as they get older and have less time to earn their way out of a share market fall.

However, age should not necessarily be the driving factor for asset allocation decisions. A 25 year-old is probably unwise to have 75% of assets in equities if they are looking to buy a house in the next two years. Equally, a 90-year-old probably should not have only 10% in equities if their lifestyle is fully funded and their children and grandchildren, who will eventually inherit their estate, have decades of investing ahead of them.

It is always wise to have a reasonable proportion of cash on hand in case of some surprise like illness or loss of job, and also to readily be able to take advantage of opportunities to buy assets when they become cheap. Benjamin Graham, the father of value investing, guided for most people to have 25% or more in bonds, or other safe investments, for most people. He believed such a cushion gives investors greater confidence to own equities when they are falling. Graham’s philosophy, shared by us, is to first preserve capital, and then help it grow.

Equally, most investors should own some shares to help portfolios withstand inflation and retirement funding needs. Equities have a record of outperforming all other asset classes over time. Even in retirement, at least some assets should be invested for the long-term. Increasing life expectancy means investors can expect to live two to three decades after retirement, increasing the importance of designing portfolios that live longer than we do.

Contact Us

Let us demonstrate how we can deliver outstanding outcomes for you.

p +61 2 8094 8410

e info@assureinvest.com.au

About AssureInvest

AssureInvest is your trusted professional investment partner. We offer a holistic and successful investment approach and carefully tailored solutions for individual needs, as well as cost saving innovations, integrity at the highest level and attentive customer service.

Our advisor clients are empowered to boost their profits and deliver better investment outcomes, benefiting their clients and the broader community.

Our disciplined and long term focus provides a critical framework for assessing new value-adding opportunities, preserving capital, generating superior returns and implementing at low cost.

Copyright

Copyright © 2016 AssureInvest Pty Ltd ABN 55 636 036 188 (AssureInvest). All rights reserved. No part of this publication may be reproduced or distributed in any form without prior consent in writing from AssureInvest.

Disclaimer

AssureInvest has taken all care in preparing this presentation and the data, information and research commentary within it (together referred to as the ‘publication’) but to the extent that the publication is based on information received from other parties no liability is accepted by AssureInvest for errors contained in the publication or omissions from the publication. AssureInvest gives neither guarantee nor warranty nor makes any representation as to the correctness or completeness of the publication. AssureInvest bases its data, information and research commentary on information disclosed to it by other parties. Past performance is no guarantee of future performance.

General Advice Warning

The information contained within this publication is of a general nature only. No information contained in the publication constitutes the provision of securities advice. AssureInvest warns that: (a) in preparing the publication, AssureInvest did not take into account the particular goals and objectives, anticipated resources, current situation or attitudes of any particular person; and (b) before making any investment decisions on the basis of that publication, any investor or prospective investor needs to consider, with or without the assistance of a securities adviser, whether the information contained within the publication is appropriate in light of the particular goals and objectives, anticipated resources, current situation or attitudes of the investor or prospective investor. If the information contained in this document relates to the possible purchase of a financial product, the client should consider the relevant product disclosure statement (PDS) before making any decision.

Disclosure

AssureInvest has no debt or equity relationship with any funds management or financial advisory group. AssureInvest may have an interest in the securities referred to in the publication in that AssureInvest and/or its staff may hold or intend to hold deposits, shares, units or other rights in respect of such products and from time to time AssureInvest may provide some of the investment product providers mentioned in the publication with research, consulting and other services for a fee.

AssureInvest Pty Ltd

ABN 55 636 036 188 AFSL number 478978.

FREE Special Report: How to Jump ahead of competitors and add more value for clients

Learn how you can boost profits while enhancing customer outcomes.